📌 UPDATE — April 22, 2026

Tesla has officially reported its Q1 2026 earnings, beating Wall Street expectations across the board. The company posted EPS of $0.41 (vs. $0.34 est.), a gross margin of 21.1% (vs. 17.7% est.), and revenue of $22.4B (vs. $21.9B est.) — significantly outpacing the consensus figures outlined below. The gross margin beat was particularly notable, coming in more than 3.5 percentage points above the original $21.4B revenue consensus we reported.

| Metric | Consensus Est. | Actual | Beat By |

|---|---|---|---|

| EPS | $0.34 | $0.41 | +$0.07 |

| Gross Margin | 17.7% | 21.1% | +3.4pp |

| Revenue | $21.9B | $22.4B | +$0.5B |

📌 UPDATE — April 22, 2026

Tesla has officially confirmed its Q1 2026 Earnings Call is underway today at 4:30 PM CT (5:30 PM ET). The call is live now — Tesla posted the official stream link on X, and community trackers like Teslascope are spotlighting expected discussion topics including Full Self-Driving (FSD) progress and Autopilot hardware updates across HW3, AI4, and AI5. Tune in via the livestream link shared by @SawyerMerritt for real-time coverage.

The News: Tesla has published its company-compiled analyst consensus for Q1 2026 earnings, setting Wall Street's benchmark ahead of the April 22 report.

Why It Matters: These figures are the official yardstick — beat them and the stock likely pops; miss them and pressure mounts on Tesla's recovery narrative.

Source: @SawyerMerritt · @wholemars

Tesla Sets the Bar Before Q1 2026 Earnings

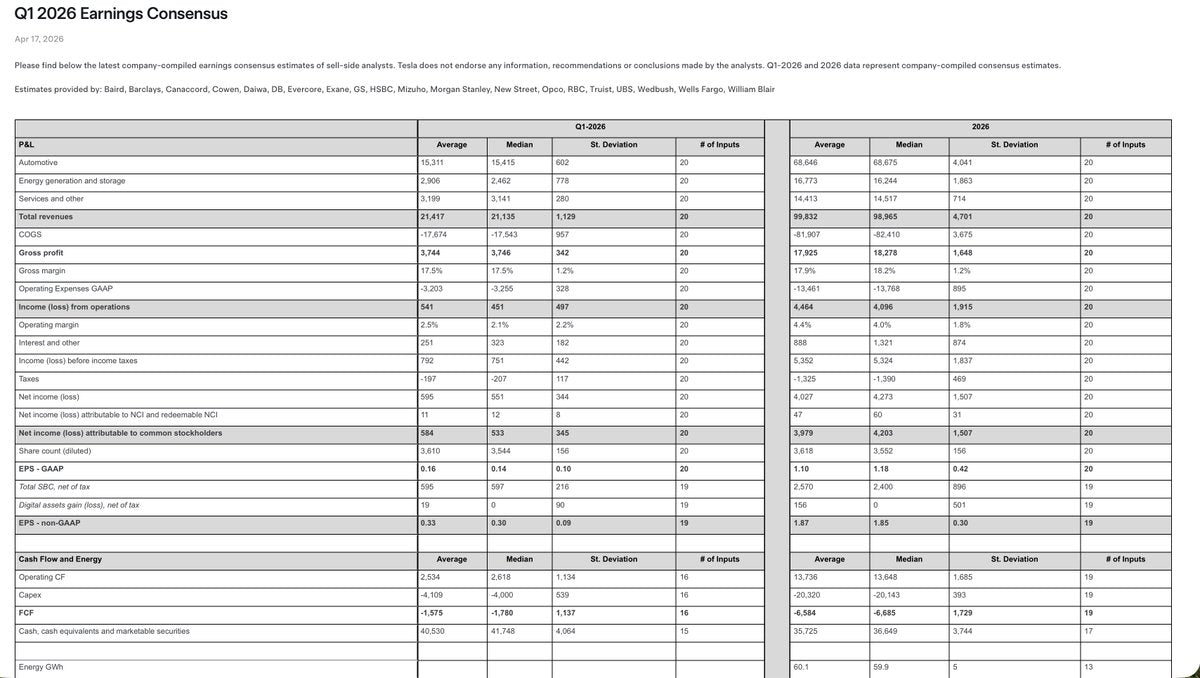

Tesla dropped its company-compiled analyst consensus on April 17, 2026 — exactly five days before it reports Q1 2026 results after market close on April 22. This is Tesla's own aggregation of Wall Street estimates, published directly on its Investor Relations page, and it's the clearest signal we have of what analysts collectively expect heading into earnings.

📊 Key Figures

| Metric | Consensus Estimate | Context |

|---|---|---|

| Total Revenue | $21.4B | ($21,417M average per Tesla IR) |

| GAAP EPS | $0.16 | Thin but positive |

| Gross Margin | 17.5% | Below peak; pricing pressure visible |

| Free Cash Flow | -$1.57B | Negative; heavy capex cycle expected |

| Earnings Date | April 22, 2026 | After market close |

Source: Tesla Investor Relations, April 17, 2026. Free cash flow figure per @SawyerMerritt; not explicitly listed in Tesla's published IR table.

🔭 The BASENOR Take

Timeline: Consensus published April 17 → Earnings report April 22 (after close)

Impact Level: 🟡 Medium — sets expectations, but the real story is whether Tesla beats or misses

Confidence: High — figures come directly from Tesla's own IR publication

📰 Deep Dive

The headline number — $21.4 billion in revenue — reflects a market that has already baked in significant headwinds for Tesla. Gross margin at 17.5% signals that analysts aren't expecting a dramatic recovery from the pricing pressure that has compressed margins over recent quarters. This is not a bar set for triumph; it's a bar set for survival, and clearing it would still require Tesla to demonstrate that its cost structure is stabilizing.

The free cash flow expectation of negative $1.57 billion is the figure that deserves the most attention. A negative FCF quarter isn't automatically alarming — Tesla is in an aggressive capital expenditure cycle, investing heavily in manufacturing expansion and next-generation product development. But it does mean the company will need to lean on its cash reserves or financing to fund operations, and investors will be watching for any commentary on when FCF is expected to turn positive again.

GAAP EPS of $0.16 is razor-thin. Any meaningful miss on revenue or a gross margin that comes in below 17% could push EPS negative, which would almost certainly trigger a sharp market reaction. Conversely, if Tesla manages to report margins above 18% — something that has happened before when cost efficiencies outpaced pricing cuts — the stock could see a significant relief rally heading into the summer.

For Tesla owners, earnings results have a direct downstream effect: strong quarters tend to give Tesla more pricing flexibility (and less pressure to cut prices to move inventory), while weak quarters historically precede aggressive incentive programs. Watch the April 22 call closely — and specifically what management says about Cybercab production timelines and energy storage deployments, both of which could be the margin-accretive stories that change the narrative.

Marcus covers Tesla's software releases, FSD rollouts, and OTA changes. Background in automotive engineering. Based in Austin.

Sources verified at publish time. Spotted an inaccuracy? Email editorial@basenor.com.