30-Second Brief

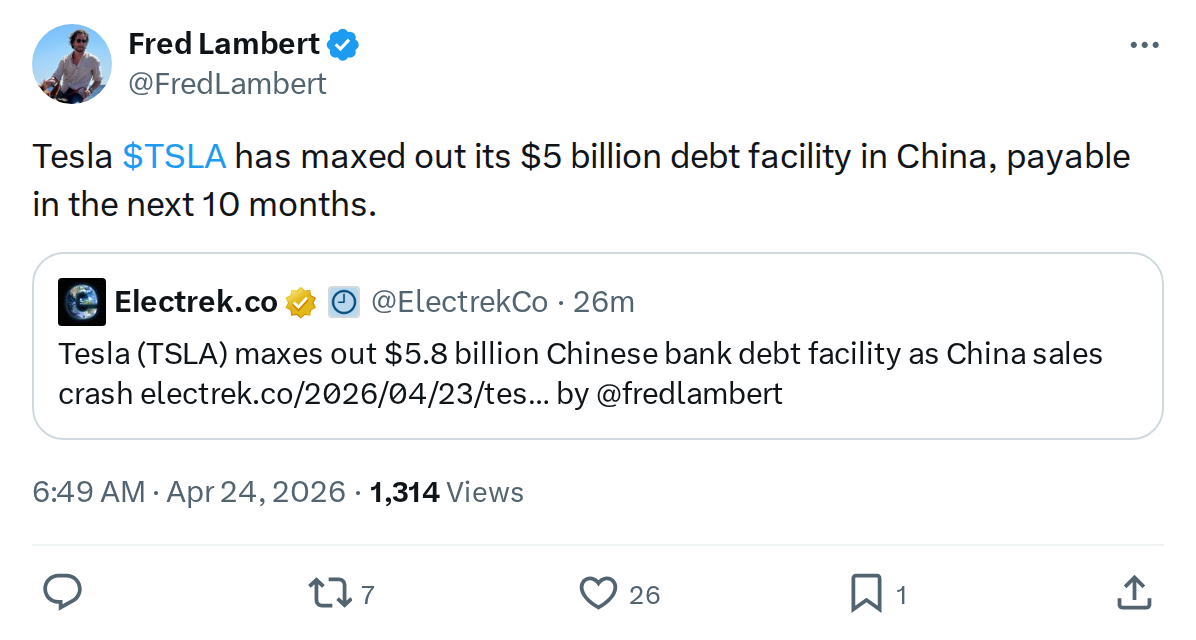

The News: Tesla has fully drawn down its China Working Capital Facility, reaching $5.8 billion (RMB 40 billion), with repayment due between September 2026 and March 2027.

Why It Matters: This is a significant balance sheet move — Tesla is leaning heavily on low-cost Chinese credit to fund its largest manufacturing operation outside the US, and the clock on repayment is already ticking.

Source: @FredLambert on X

Tesla Fully Draws $5.8 Billion China Debt Facility — Repayment Due Within 10 Months

April 23, 2026 • Tesla News • 5 min read

Tesla has maxed out its China Working Capital Facility, fully drawing down the entire RMB 40 billion ($5.8 billion) credit line, according to the company's Q1 2026 10-Q filing. With all outstanding borrowings set to mature between September 2026 and March 2027, this is one of the most consequential near-term financial obligations on Tesla's books right now.

📊 Key Figures

| Metric | Value | Context |

|---|---|---|

| Total Facility Size | $5.8B (RMB 40B) | Fully drawn as of Q1 2026 |

| Original Facility (Apr 2024) | $2.8B (RMB 20B) | Unsecured revolving credit |

| Expansion (Sep 2025) | +$2.7B (RMB 20B) | Doubled the original line |

| Interest Rate | ~2.01–2.11% | PBOC LPR minus 0.89–0.99% |

| Maturity Window | Sep 2026 – Mar 2027 | ~10 months from now |

| Availability Extended Through | April 2028 | Amended March 2025 |

How This Facility Evolved

The China Working Capital Facility didn't start at $5.8 billion. Tesla established it in April 2024 as an unsecured revolving credit line worth RMB 20 billion — roughly $2.8 billion at the time. That alone was a substantial commitment, reflecting Tesla's need for flexible working capital to support Gigafactory Shanghai's production and supply chain operations.

Then in September 2025, Tesla doubled down — literally. The facility was expanded by an additional RMB 20 billion, bringing the total commitment to RMB 40 billion (approximately $5.5–5.8 billion at current exchange rates). By the time Q1 2026 closed on March 31, every dollar of that expanded facility had been drawn.

One important nuance: in March 2025, Tesla amended the facility to extend the availability of funds through April 2028. That means Tesla has runway to re-borrow after repayment — this isn't a one-time credit line that disappears after the maturity dates hit.

Why the Interest Rate Matters

At roughly 2.01–2.11% annually, this is exceptionally cheap debt. The rate is calculated as the People's Bank of China's Loan Prime Rate minus a preferential spread of 0.89–0.99%. For context, US corporate borrowing rates have been significantly higher. Tesla is effectively accessing Chinese state-backed financial infrastructure at near-sovereign rates — a strategic advantage that helps fund Gigafactory Shanghai's operations without putting pressure on US-side liquidity.

This preferential rate also signals something about Tesla's relationship with Chinese financial institutions and, by extension, the Chinese government. Securing a $5.8 billion unsecured revolving credit line at sub-2.2% interest isn't available to just any foreign automaker operating in China.

🔭 The BASENOR Take

Timeline: Facility established April 2024 → expanded September 2025 → fully drawn by March 31, 2026 → repayment due September 2026–March 2027

Impact Level: 🟠 Significant — $5.8B in near-term obligations is material, but the facility's renewal terms reduce refinancing risk

Confidence: ✅ High — confirmed in Tesla's Q1 2026 10-Q SEC filing

The headline — "Tesla maxes out $5B China debt" — sounds alarming at first read. But the fuller picture is more nuanced. This is working capital financing, not distress borrowing. Tesla is using cheap Chinese credit to fund the day-to-day operations of its highest-volume factory, which produced over 700,000 vehicles in 2024 alone.

The real question is what happens between now and March 2027. Tesla has three realistic paths: repay from operating cash flow generated by Gigafactory Shanghai itself, refinance under the extended availability window (which runs through April 2028), or some combination of both. Given that the facility was expanded — not reduced — as recently as September 2025, Tesla's Chinese banking partners appear confident in the company's creditworthiness.

For Tesla owners, the more relevant signal here is strategic: Tesla is deeply embedded in China's financial system, not just its manufacturing base. That creates both resilience (access to low-cost capital) and exposure (geopolitical risk if US-China trade tensions escalate further). With tariffs already reshaping the global auto industry in 2025–2026, the timing of this repayment window is worth watching.

📰 Deep Dive

Fully drawing a $5.8 billion credit facility isn't unusual for a company running a massive manufacturing operation — but the speed of utilization is notable. Tesla went from establishing a $2.8 billion line in April 2024 to drawing down a $5.8 billion expanded version by March 2026. That's roughly 24 months to double and fully exhaust the facility. It suggests Tesla's China operations are consuming working capital at a pace that even a multi-billion dollar credit line struggles to keep ahead of.

Gigafactory Shanghai is Tesla's most efficient production site and its primary export hub for markets across Europe and Asia-Pacific. The working capital demands of running that scale of operation — supplier payments, logistics, inventory, local payroll — are enormous. Tapping Chinese credit at 2% to fund those operations, rather than repatriating US dollars or issuing equity, is a financially rational decision.

What bears watching over the next 10 months is whether Tesla refinances smoothly or faces any friction. The March 2025 amendment extending availability through April 2028 was a smart hedge — it means Tesla can roll the debt forward even if market conditions shift. But if US-China trade relations deteriorate significantly before the maturity window closes, the calculus could change. Tesla's Q2 and Q3 2026 earnings calls will be the place to watch for any updates on how management is handling this obligation.

From a pure credit perspective, $5.8 billion at ~2.1% is roughly $120 million in annual interest — a manageable figure for a company of Tesla's scale. The risk isn't the interest burden; it's the refinancing or repayment execution in a potentially volatile geopolitical environment. That's the thread worth pulling on as this story develops.

David covers the EV industry, regulatory developments, and accessory ecosystem. 15+ years writing about consumer tech. Based in London.

Sources verified at publish time. Spotted an inaccuracy? Email editorial@basenor.com.