The News: Analyst Whole Mars Catalog estimates Tesla's fast charging network is generating approximately $900 million per quarter — a $3.6 billion annual run rate.

Why It Matters: The Supercharger network is quietly becoming one of Tesla's most significant revenue engines, with Bloomberg projecting it could reach $7.4 billion annually by 2030.

Source: @wholemars on X

Tesla's Supercharger Network Is Now a $3.6 Billion Business — And It's Just Getting Started

Tesla's Supercharger network has long been celebrated as the gold standard in EV charging infrastructure. But the financial story behind it is only now coming into full focus. Whole Mars Catalog — one of the sharper independent Tesla analysts on X — dropped a notable estimate today: Tesla is generating roughly $900 million per quarter in fast charging revenue, implying a $3.6 billion annual run rate.

This isn't an official Tesla figure — Tesla doesn't break out Supercharging revenue as a standalone line item. But the estimate is grounded in real, verifiable data points, and it paints a picture of a charging business that has quietly become a major financial asset.

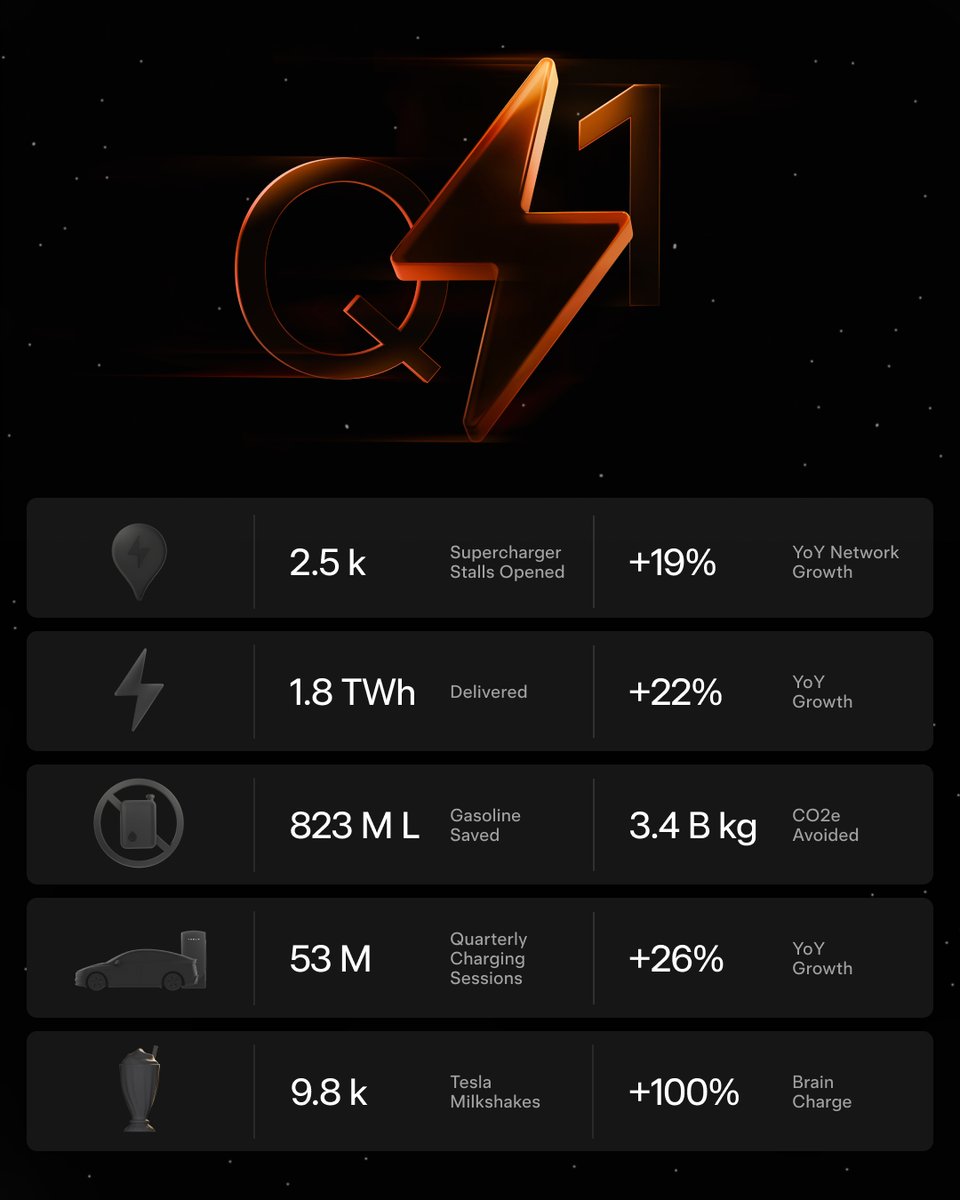

📊 Key Figures

| Metric | Value | Context |

|---|---|---|

| Estimated Annual Run Rate | $3.6B | Per @wholemars estimate |

| Estimated Quarterly Revenue | ~$900M | Per @wholemars estimate |

| 2025 Services & Other Revenue | $12.53B | +19% YoY (includes Supercharging) |

| Q2 2025 Services & Other Revenue | $3.0B | Up from $2.61B in Q2 2024 |

| 2025 Energy Delivered | 6.7 TWh | Record; includes non-Tesla EVs |

| Q4 2025 Charging Sessions | ~52M | Global sessions in Q4 alone |

| Global Supercharger Stalls (end 2025) | 77,682 | +19% YoY; 8,182 stations |

| Bloomberg 2030 Revenue Projection | $7.4B | Projected annual revenue |

How Did We Get Here?

The Supercharger network's rise as a revenue center is the product of two converging forces: explosive network growth and the strategic opening of the network to non-Tesla vehicles.

By the end of 2025, Tesla had surpassed 77,600 Supercharger stalls across more than 8,100 stations globally — a 19% year-over-year increase in connectors. More importantly, the network delivered a record 6.7 terawatt-hours of electricity throughout 2025, including energy consumed by non-Tesla EVs. That last detail matters enormously. When Tesla adopted NACS as the North American standard and opened its network, it didn't just do the EV industry a favor — it turned its charging infrastructure into what analysts have started calling a toll booth for every EV on the road.

In Q4 2025 alone, the network handled approximately 52 million charging sessions. At even modest average revenue per session, the math starts to validate Whole Mars Catalog's $900 million quarterly estimate.

Putting the Numbers in Perspective

Tesla doesn't report Supercharging as a standalone revenue line. It's bundled into the company's "Services and Other" segment, which generated $12.53 billion in 2025 — up 19% year-over-year. Paid Supercharging sessions were explicitly cited by Tesla as a primary driver of that growth, alongside maintenance, collision, used vehicle sales, and insurance revenue.

For context, Bloomberg estimated Tesla's charging network revenue at approximately $1.74 billion back in 2023. If the Whole Mars Catalog estimate of $3.6 billion annually is in the right ballpark for 2026, that would represent more than a doubling of charging revenue in roughly three years — consistent with the network's documented growth trajectory.

📈 Revenue Growth Trajectory

| 2023 (Bloomberg estimate) | ~$1.74B/year |

| 2026 (Whole Mars Catalog estimate) | ~$3.6B/year |

| 2030 (Bloomberg projection) | $7.4B/year |

🔭 The BASENOR Take

Timeline: Estimate published April 1, 2026 | Q1 2026 earnings due April 21, 2026

Impact Level: High — reframes how the market should value Tesla's infrastructure assets

Confidence: Medium — estimate is analyst-derived, not official Tesla disclosure; directionally consistent with verified data

The Whole Mars Catalog estimate deserves serious attention, even if it can't be independently verified until Tesla provides more granular disclosure. Here's why: every data point we can verify — TWh delivered, session counts, network growth rates, and the Services segment's overall trajectory — points in the same direction. The Supercharger network is scaling faster than most people realize, and its economics are improving as utilization rises.

The NACS adoption story is the underappreciated accelerant here. Every non-Tesla EV that plugs into a Supercharger is pure incremental revenue on infrastructure Tesla has already built and paid for. The marginal cost of an additional charging session is essentially just electricity — and Tesla is charging a premium for the reliability and convenience its network delivers.

What should owners watch for? The April 21 Q1 2026 earnings call is the next real data point. Tesla rarely breaks out Supercharging revenue explicitly, but management commentary on the Services segment — and any mention of charging session volumes or energy delivered — will help calibrate how close the $3.6 billion estimate really is. If the Services segment continues its 19% growth trajectory, the math gets very interesting very quickly.

For the long-term picture: Bloomberg's $7.4 billion projection by 2030 would make the Supercharger network, on its own, a business larger than many Fortune 500 companies. That's not a side hustle. That's a strategic asset that fundamentally changes how Tesla should be valued — and how owners should think about the infrastructure they're paying into every time they charge.

Marcus covers Tesla's software releases, FSD rollouts, and OTA changes. Background in automotive engineering. Based in Austin.

Sources verified at publish time. Spotted an inaccuracy? Email editorial@basenor.com.