SpaceX went public in June 2026 and immediately became one of the most talked-about stocks on the market. But with a $1.8 trillion market cap and no projected profits until 2027, at least one prominent analyst is asking a pointed question: what exactly are investors paying for? Here's a breakdown of the key valuation questions every Tesla — and SpaceX — watcher should understand.

How did SpaceX get a $1.8 trillion valuation so fast?

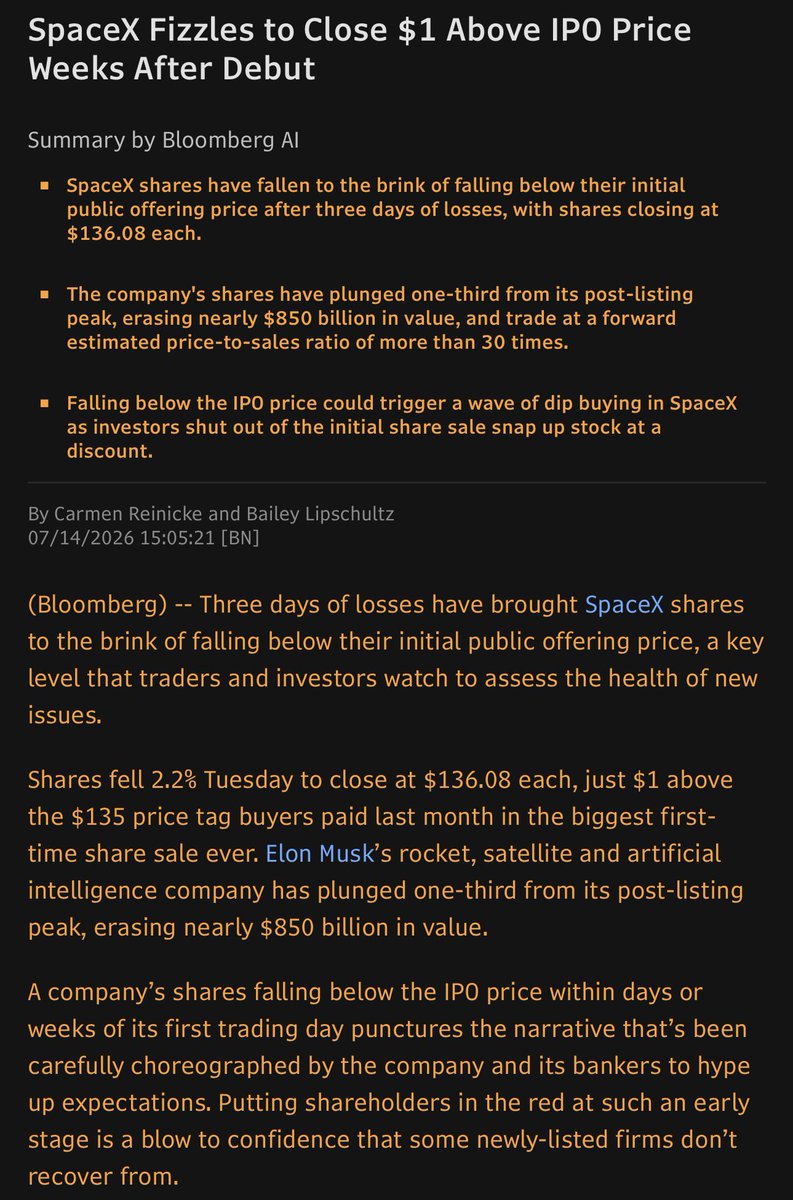

SpaceX completed its IPO on the Nasdaq on June 12, 2026, pricing shares at $135 each and raising approximately $75–86 billion — one of the largest public offerings in history. At listing, the company was valued at roughly $1.77 trillion. Shares surged immediately after trading opened, briefly pushing the market cap above $2 trillion before settling back. To put that trajectory in context: SpaceX was valued at around $350 billion in a private secondary transaction as recently as December 2024. The xAI merger in February 2026, valued at $1.25–1.5 trillion, was a major catalyst. The IPO effectively crystallized years of private-market enthusiasm into a single, very large public number.

What does Gary Black's skepticism actually rest on?

Gary Black, a closely followed institutional investor and Tesla analyst, flagged three specific concerns. First, at $1.8 trillion, SpaceX is already a megacap — the kind of company where meaningful upside requires either enormous revenue growth or a dramatic multiple expansion, both of which are harder to achieve at scale. Second, SpaceX is not expected to generate profits until 2027, meaning investors are paying a premium today for earnings that don't yet exist. Third, and most striking, SpaceX trades at 47x its 2026 estimated EV/Revenue — more than three times Tesla's 14x multiple on the same metric.

How do the valuation multiples actually compare to Tesla?

The numbers Black cites are worth looking at side by side. On an EV/Revenue basis, SpaceX at 47x dwarfs Tesla at 14x — meaning the market is pricing in far more future growth per dollar of current revenue for SpaceX than it does for Tesla. On EV/EBITDA, the gap narrows but remains significant: SpaceX at 110x versus Tesla at 97x. Tesla itself is not considered a cheap stock by traditional metrics, so the fact that SpaceX trades at a meaningful premium to Tesla on both measures is a signal worth taking seriously. SpaceX reported $18.7 billion in revenue in 2025 (up 33% year-over-year), with Starlink accounting for $11.4 billion of that total — a strong growth story, but one the market appears to have already priced in aggressively.

What is the bull case that Black acknowledges?

Black's post was cut off mid-sentence — he noted he "gets the TAM story" before the tweet truncated. That's a reference to Total Addressable Market: the argument that Starlink's global broadband ambitions, Starship's potential to dominate heavy-lift launch economics, and point-to-point Earth transportation represent markets large enough to justify today's premium. Supporters of the valuation point to Starlink's rapid subscriber growth and the near-monopoly SpaceX holds in commercial launch services. The bull thesis is essentially that SpaceX is building infrastructure-level businesses that will look cheap in a decade — the same argument that was made about Tesla's energy and autonomous driving segments years ago.

What does this mean for Tesla investors specifically?

For owners and investors who hold $TSLA, the SpaceX IPO creates an interesting dynamic. Capital that might have flowed into Tesla — particularly from investors who want Elon Musk exposure — now has an alternative home. Whether that represents meaningful competition for Tesla's shareholder base, or simply expands the overall pie of Musk-adjacent investment, remains to be seen. What's clear is that the market is currently assigning a higher growth premium to SpaceX than to Tesla, despite Tesla's more established revenue base, its FSD and robotaxi roadmap, and its Optimus manufacturing ambitions. Whether that premium is justified depends almost entirely on how quickly SpaceX can convert its TAM narrative into actual earnings — and 2027 is the year the market will start demanding answers.

Related Gear

Gear up your Tesla with tested, custom-fit BASENOR accessories — shop Tesla accessories →

Sarah focuses on Tesla Energy, SpaceX missions, and the broader Musk AI portfolio. Former data analyst in clean energy. Based in San Francisco.

Sources verified at publish time. Spotted an inaccuracy? Email editorial@basenor.com.