X Money appears to be entering a broader rollout phase, with multiple prominent accounts reporting access to the integrated payment feature on June 29. The service — which officially went live for US Premium and Premium+ subscribers on June 26, according to verified reports — is quietly becoming one of the most significant expansions of Elon Musk's platform beyond social media.

Notably, @wholemars floated an interesting theory: receiving a payment from another user may trigger access. That suggests X could be using peer-to-peer activity as an organic activation mechanism — spreading the feature through actual use rather than a traditional waitlist.

Here are six things worth knowing as X Money expands.

1. It Went Live for Premium Subscribers on June 26

According to multiple verified reports, X Money officially launched for US Premium and Premium+ subscribers on June 26, 2026. Early public access had been previewed in April. A full rollout to all US users is targeted for mid-2026, though no confirmed completion date has been announced. The feature is US-only for now — and notably unavailable in New York and Massachusetts pending additional regulatory approvals.

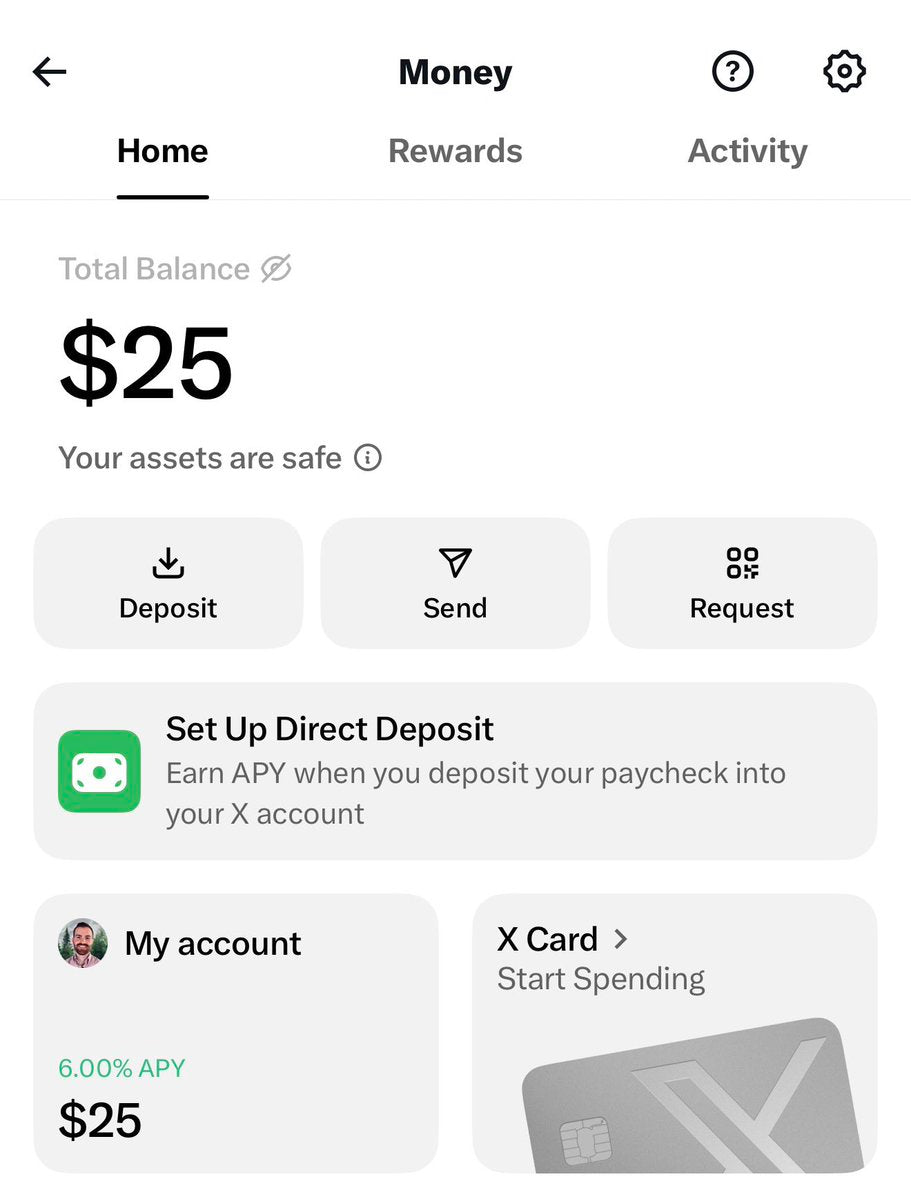

2. It's a Full Digital Wallet, Not Just Tipping

X Money isn't a simple tip jar. It functions as a digital wallet with peer-to-peer transfers to any @handle via Visa Direct, a USD balance you can hold inside the app, direct deposit support, and bill pay functionality. Think less "social media tip feature" and more "a bank account that lives inside your timeline."

3. The Debit Card Is Metal and Bears Your Username

Users who sign up receive a personalized metal Visa debit card stamped with their X username — a detail that underscores how seriously X is positioning this as a primary financial product, not a novelty add-on. The card carries 3% cashback on purchases and zero foreign transaction fees, according to published feature details.

4. Deposits Earn ~6% APY With No Minimum Balance

X Money advertises approximately 6% Annual Percentage Yield on fiat deposits held in the wallet — with no minimum balance required to earn interest. That rate is meaningfully higher than most traditional savings accounts. Deposits are held by Cross River Bank, an FDIC member based in Fort Lee, NJ, and X's cash sweep program distributes balances across partner banks to offer up to $10 million in FDIC coverage per user.

5. X Has Secured Money Transmitter Licenses in 40+ States

The regulatory groundwork has been substantial. X holds Money Transmitter Licenses in over 40 US states and Washington, D.C. The two notable holdouts — New York and Massachusetts — are the primary reason the service isn't yet universally available. Elon Musk has previously indicated that New York approval could come soon, which would open the feature to one of the largest US user bases.

6. Crypto Is Not Part of the Initial Launch

Despite longstanding speculation about Bitcoin or Dogecoin integration, the initial X Money rollout focuses exclusively on fiat transactions and P2P payments. Crypto functionality has not been included at launch. Whether that changes in a future update remains an open question — but for now, X Money is a conventional digital banking product built on top of a social platform.

The peer-activation theory from @wholemars is worth watching closely. If receiving a payment genuinely unlocks access, the feature could spread rapidly through X's most active financial communities without any formal announcement — exactly the kind of organic, word-of-mouth expansion that makes a payments network self-reinforcing from day one.

Sarah focuses on Tesla Energy, SpaceX missions, and the broader Musk AI portfolio. Former data analyst in clean energy. Based in San Francisco.

Sources verified at publish time. Spotted an inaccuracy? Email editorial@basenor.com.