The News: Bank of America has resumed coverage on Tesla ($TSLA) with a Buy rating and a $460 price target, explicitly naming FSD the "leading consumer autonomy solution."

Why It Matters: A major Wall Street firm is now putting hard numbers behind Tesla's autonomy bet — and the math suggests robotaxi services alone could account for more than half of Tesla's total valuation.

Source: @SawyerMerritt on X

📊 Key Figures

| Metric | Value | Context |

|---|---|---|

| BofA Price Target | $460 | +17.2% upside from $392.43 |

| Previous BofA Rating | Neutral | Upgraded to Buy |

| Robotaxi % of Valuation | ~52% | Of BofA's total TSLA valuation |

| Optimus Division Value | >$30B | BofA sum-of-the-parts estimate |

| Energy Division Value | $90B | BofA sum-of-the-parts estimate |

| FSD Cumulative Miles | 8.4B+ | Worldwide as of March 2, 2026 |

| Robotaxi Expansion (H1 2026) | +7 markets | Beyond current SF & Austin ops |

Why Wall Street Is Paying Attention to FSD Now

Bank of America's reinstatement isn't just a routine rating change — it's a substantive argument about where Tesla's value actually lives. The firm's analysts didn't lead with vehicle deliveries or margins. They led with FSD and autonomy.

The core of BofA's thesis is that Tesla's camera-only autonomous driving architecture — the same system in your car right now — is technically harder to build than multi-sensor approaches, but it scales far more cheaply. No lidar. No radar arrays. Hardware that's already in millions of vehicles on the road today. That cost efficiency, BofA argues, is what positions Tesla to dominate robotaxi economics in a way no other player currently can.

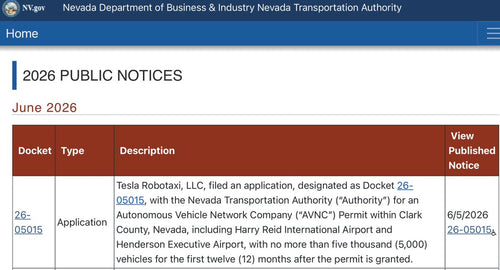

The firm's robotaxi services are currently operating in San Francisco and Austin, with plans to expand to seven additional markets in the first half of 2026, according to BofA's research. That's a rapid deployment timeline — and it's the engine behind the bank's estimate that robotaxi services alone could represent approximately 52% of Tesla's total valuation.

The Sum-of-the-Parts Picture

BofA's analysis breaks Tesla into distinct business units rather than treating it as a single automaker. That framing matters. When you value Tesla's energy operations at $90 billion and its Optimus humanoid division at over $30 billion — before even touching the core auto business — the $460 price target starts to look less like optimism and more like arithmetic.

For owners, this is validation that the technology you're already using — FSD (Supervised), which has now surpassed 8.4 billion cumulative miles driven worldwide — is being treated by institutional investors as a genuine competitive moat, not a marketing feature. Every mile you drive contributes to a dataset that BofA believes no competitor can replicate at scale.

🔭 The BASENOR Take

Timeline: Coverage reinstated March 4, 2026 | Robotaxi expansion to 7 new markets targeted H1 2026

Impact Level: 🟡 Moderate-High — Institutional validation of FSD's commercial trajectory

Confidence: High — BofA is a primary source with a detailed sum-of-the-parts model, not a speculative call

Analysis: The shift from Neutral to Buy, anchored specifically on FSD and robotaxi economics rather than vehicle volume, signals a broader Wall Street recalibration of how Tesla gets valued. If the robotaxi thesis holds — and BofA is betting it will — the FSD subscription and hardware you already own could become the most valuable thing about your Tesla. For owners on the fence about FSD, this is the institutional argument that the technology is real, scaling, and increasingly hard to compete with. Follow our FSD coverage as the robotaxi expansion unfolds.

📰 Deep Dive

What makes this BofA note notable is its specificity. Analyst upgrades often rely on broad macro tailwinds or valuation multiples. This one is built around a technical argument: that camera-only autonomy, while harder to engineer, produces a structurally lower cost-per-mile than sensor-fusion approaches. If that argument is correct, it means Tesla's margin advantage in robotaxi operations compounds over time as the fleet grows — without requiring expensive hardware retrofits.

The 8.4 billion cumulative FSD miles figure is the data point that underpins everything. That's not just a marketing number — it's the training signal that makes each subsequent software generation more capable. BofA is essentially arguing that this data flywheel is now wide enough and fast enough that closing the gap would require years and billions from any would-be competitor.

The robotaxi expansion timeline is the near-term test. Seven new markets in the first half of 2026 is an aggressive target. Execution — safety record, regulatory approvals, rider experience — will determine whether BofA's 52% robotaxi valuation holds up or gets revised. Tesla owners in those expansion markets will be among the first to see whether the commercial product matches the institutional thesis.

For now, the signal from one of Wall Street's largest banks is clear: FSD isn't a feature. It's the business.

Marcus covers Tesla's software releases, FSD rollouts, and OTA changes. Background in automotive engineering. Based in Austin.

Sources verified at publish time. Spotted an inaccuracy? Email editorial@basenor.com.