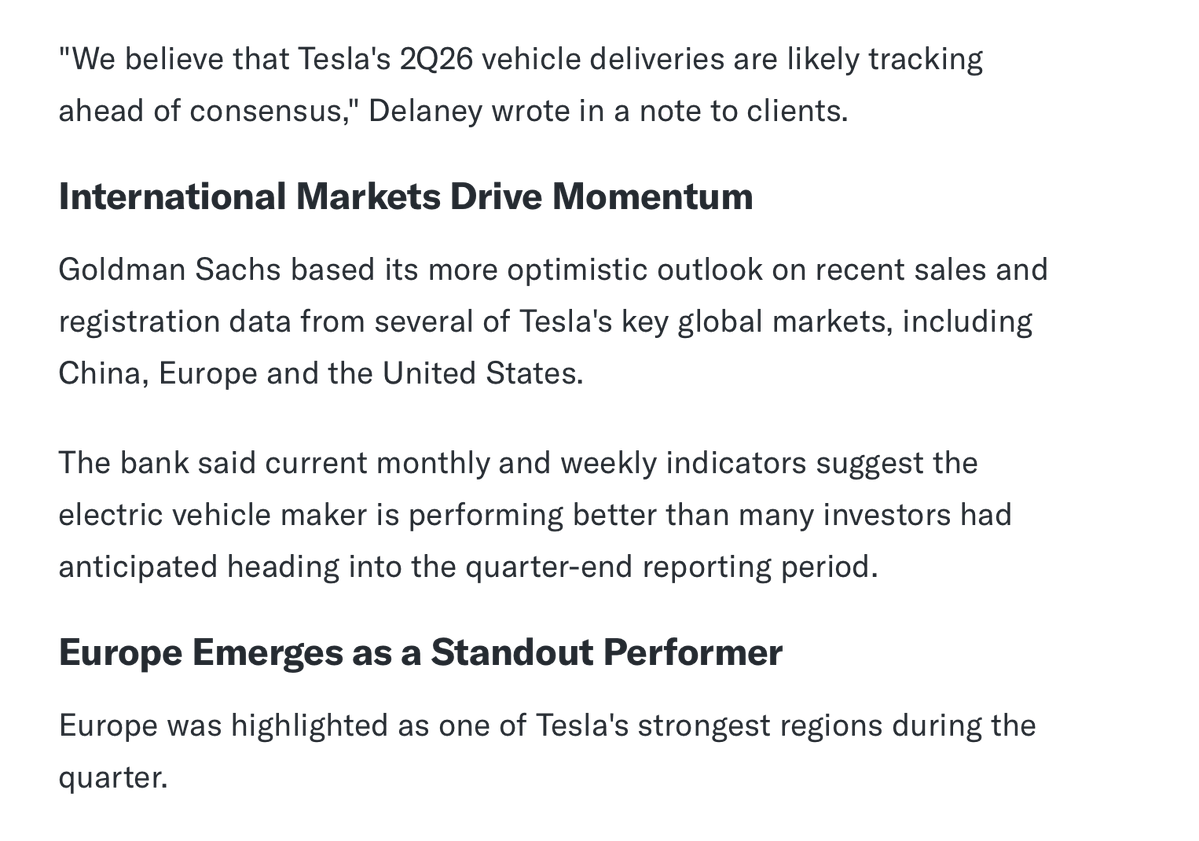

Goldman Sachs raised its Tesla delivery forecast for Q2 2026 on Monday, bumping the estimate from 405,000 to 420,000 vehicles — 5% above the Wall Street consensus of 400,000. The bank cited strong registration data across international markets as evidence that deliveries are tracking ahead of expectations, while flagging a notable soft spot in the U.S.

What Goldman Actually Said

The bank's research note, published June 16, stated that "Tesla's 2Q26 vehicle deliveries are likely tracking ahead of consensus." The upward revision was driven by strong year-over-year registration growth in Europe — up roughly 85–90% through May — along with solid momentum in China, South Korea, and Australia. That international strength was enough to offset continued weakness in the domestic market, where U.S. deliveries through May were reportedly tracking down by a mid-double-digit percentage year-over-year.

The full-year 2026 forecast was nudged up from 1.72 million to 1.73 million vehicles. Goldman also raised its 2026 earnings per share estimate (inclusive of stock-based compensation) from $1.30 to $1.35. Forecasts for 2027 and 2028 were left unchanged at 1.88 million and 1.96 million units, respectively.

| Metric | Prior Estimate | Revised Estimate |

|---|---|---|

| Q2 2026 Deliveries | 405,000 | 420,000 |

| Full-Year 2026 Deliveries | 1.72M | 1.73M |

| 2026 EPS (incl. SBC) | $1.30 | $1.35 |

| 2027 Deliveries | 1.88M | 1.88M (unchanged) |

| 2028 Deliveries | 1.96M | 1.96M (unchanged) |

The International Story vs. the U.S. Reality

The geographic split inside this revision is worth paying attention to. Europe's near-doubling of registrations year-over-year through May is a meaningful reversal from the turbulence Tesla faced in early 2025, when brand sentiment in several European markets took a hit. A recovery of that magnitude, sustained through the first five months of the year, suggests the Model Y Juniper refresh and competitive pricing have landed well across the Atlantic.

The U.S. picture is a different story. A mid-double-digit year-over-year decline domestically is a real headwind, and it's notable that Goldman's bullish Q2 revision is being carried almost entirely by markets outside North America. Whether that U.S. softness is a temporary demand dip, a pricing issue, or something tied to broader consumer sentiment will be one of the more closely watched data points when Tesla reports official Q2 numbers — expected in early July.

Neutral Rating Held

Despite the upward revisions, Goldman Sachs kept its rating on Tesla stock at Neutral and left its 12-month price target unchanged at $375. That combination — better near-term delivery numbers, higher EPS estimate, same rating and price target — signals the bank sees the Q2 beat as already priced in rather than a catalyst for a re-rating. Investors looking for a bullish turn from Goldman will have to wait for something more structural to shift the thesis.

Q2 deliveries will be reported in the first days of July. If Goldman's 420,000 estimate proves accurate — or conservative — expect the conversation around Tesla's full-year trajectory to shift quickly. The real question is whether U.S. demand finds its footing in the second half of the year, or whether international markets continue to carry the load.

David covers the EV industry, regulatory developments, and accessory ecosystem. 15+ years writing about consumer tech. Based in London.

Sources verified at publish time. Spotted an inaccuracy? Email editorial@basenor.com.