The News: Tesla posted a 6% year-over-year sales increase in Q1 2026, while legacy automakers collectively fell 19% in the same period.

Why It Matters: The gap between Tesla and traditional automakers is widening — and this quarter's numbers make that clearer than ever.

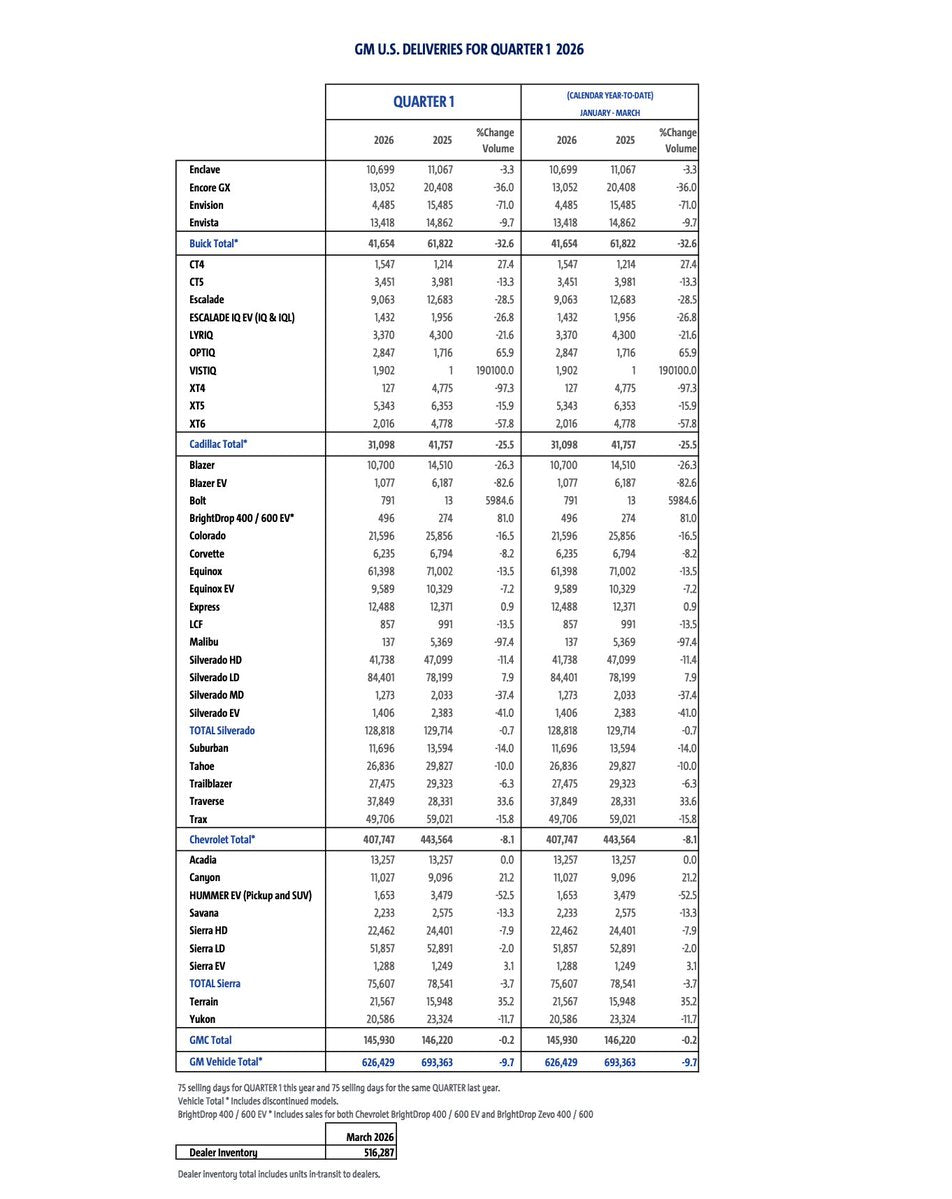

Source: @wholemars on X

Tesla Grows While Legacy Auto Stumbles in Q1 2026

Tesla's Q1 2026 results are in, and the contrast with the rest of the auto industry is stark. While traditional automakers collectively posted a 19% year-over-year decline in sales, Tesla moved in the opposite direction — up 6% year-over-year, delivering 358,023 vehicles in the quarter according to Tesla's official April 2 release.

That's not just a good quarter. That's a structural divergence playing out in real time.

📊 Key Figures

| Metric | Value | vs Q1 2025 |

|---|---|---|

| Tesla Q1 2026 Deliveries | 358,023 | +6% YoY |

| Legacy Auto (collective) | — | −19% YoY |

| Full Financial Results (earnings) | April 22, 2026 | Pending |

🔭 The BASENOR Take

Timeline: Q1 2026 delivery data released April 2, 2026. Full earnings call scheduled April 22, 2026.

Impact Level: 🟢 High — confirms Tesla's competitive positioning heading into 2026

Confidence: ✅ High — delivery figures sourced directly from Tesla's official release

A 25-percentage-point swing between Tesla and legacy auto in a single quarter is not noise. It's signal. The traditional auto industry is dealing with a compounding set of headwinds — slowing consumer demand for ICE vehicles, ongoing EV transition costs, and supply chain pressures — while Tesla continues to benefit from a vertically integrated model and a product lineup that has seen meaningful refreshes over the past 12 months.

The Model Y Juniper refresh, which rolled out globally through late 2024 and into 2025, appears to still be driving sustained demand. Combined with continued Model 3 Highland momentum and growing Cybertruck volumes, Tesla's diverse-but-focused lineup is holding up where others are faltering.

Worth noting: the 358,023 delivery figure represents the floor of what Tesla will report financially. Full revenue, margins, and net income won't be known until the April 22 earnings call. Given Tesla's history of margin pressure from price adjustments and product mix shifts, the delivery growth is encouraging — but the profitability story will be the one to watch.

📰 Deep Dive

The 19% collective decline among legacy automakers reflects more than a bad quarter — it reflects an industry mid-transition, caught between declining ICE demand and EV investments that haven't yet scaled to profitability. For Tesla, that environment is an opportunity. Every point of market share that shifts away from traditional brands is a potential Tesla buyer, and Q1 2026 suggests that dynamic is accelerating.

Tesla's 6% YoY growth is also notable in context: the company is growing off an already large base. Scaling deliveries at this rate, while simultaneously investing in next-generation platforms like the Cybercab and expanding Gigafactory capacity, is operationally difficult. That it's happening while competitors shrink makes it more significant.

The April 22 earnings call will be the real test. Investors and owners alike will be watching gross margins closely — if Tesla maintained or improved margins while growing volume, that's a fundamentally stronger business story than growth achieved through aggressive discounting. Either way, Q1 2026 has already told us something important: in a down market for the broader auto industry, Tesla is moving in a different direction entirely.

David covers the EV industry, regulatory developments, and accessory ecosystem. 15+ years writing about consumer tech. Based in London.

Sources verified at publish time. Spotted an inaccuracy? Email editorial@basenor.com.