📌 UPDATE — April 22, 2026

Tesla's CFO delivered a mixed forward outlook on the Q1 earnings call: the company expects negative free cash flow for the remainder of 2026 and is projecting a massive $25 billion in CapEx over the next year — signaling heavy investment ahead. On the demand side, however, the picture is strikingly bullish: Tesla says it exited Q1 with the largest auto order backlog in its history, with the CFO citing "a huge surge in demand around the world" to start 2026. Additionally, net income took a hit from Bitcoin mark-to-market losses, adding another layer to the one-time items already shaping this quarter's headline numbers.

30-Second Brief

The News: Tesla's Q1 2026 earnings report, released today, shows operating income surged 136% year-over-year — but the primary driver was one-time tariff-related benefits, not organic business growth.

Why It Matters: Strip out those one-time items and Tesla's underlying profitability picture looks considerably more complicated — especially with vehicle deliveries down ~7% year-over-year.

Source: @FredLambert on X

Tesla Q1 2026 Earnings: A Tariff Windfall Masked the Real Story

Tesla dropped its Q1 2026 earnings report after market close today, and the headline numbers look impressive. But dig one layer deeper and a critical question emerges — one that Electrek editor Fred Lambert raised immediately: how much of Tesla's profit surge was driven by a one-time tariff refund, rather than genuine operational improvement?

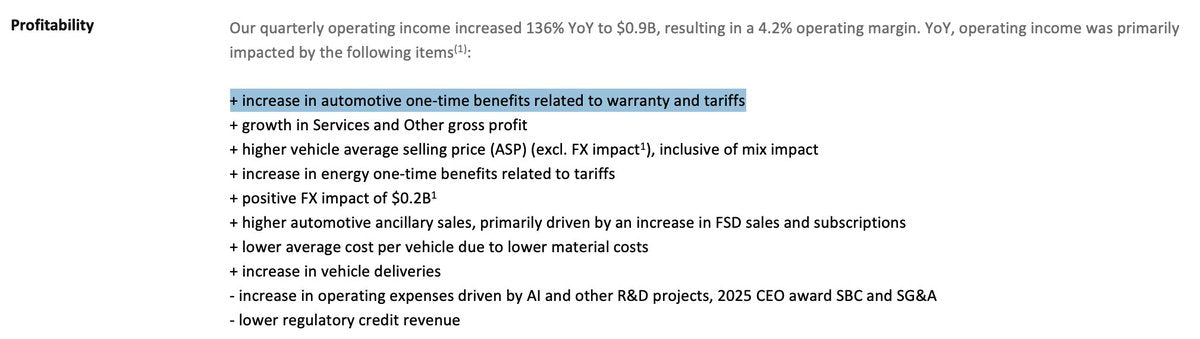

It's the right question to ask. Tesla's own earnings materials acknowledged that the jump in operating income — from $399 million in Q1 2025 to $941 million in Q1 2026 — was primarily driven by "automotive one-time benefits related to warranty and tariffs" and "energy one-time benefits related to tariffs." The company did not disclose the specific dollar value of these benefits.

📊 Key Figures

| Metric | Q1 2026 | vs Q1 2025 |

|---|---|---|

| Total Revenue | $22.38B | +16% |

| Operating Income | $941M | +136% ⚠️ |

| GAAP Net Income | $477M | +17% |

| Non-GAAP Net Income | $1.45B | +56% |

| Adjusted EPS | $0.41 | +51% |

| Gross Margin | 21.1% | — |

| Vehicle Deliveries | 358,023 | −7% YoY |

| Vehicle Production | 408,386 | — |

⚠️ Operating income growth was primarily attributed to one-time tariff and warranty benefits per Tesla's own earnings materials.

The Tariff Refund Question — What We Know

The tariff benefit referenced in Tesla's earnings is likely tied to an estimated $175 billion in refunds for IEEPA (International Emergency Economic Powers Act) tariffs, following a Supreme Court ruling in February 2026. The U.S. Customs refund portal for these tariffs only launched on April 20, 2026 — just two days before Tesla's earnings release.

This timing raises a legitimate question: did Tesla receive — or accrue — an early tariff refund that was booked into Q1 results? Tesla's disclosure that one-time tariff benefits were the primary driver of operating income improvement suggests the answer is yes, at least in part. But without a specific dollar figure from Tesla, the exact magnitude remains opaque.

⚠️ What Tesla Did — and Didn't — Disclose

- Disclosed: One-time tariff and warranty benefits were the primary driver of operating income improvement

- Disclosed: Both automotive and energy segments saw tariff-related one-time benefits

- Not disclosed: The specific dollar value of these one-time tariff benefits

- Not disclosed: Whether these benefits are expected to recur in future quarters

What Actually Drove — and Dragged — the Quarter

Beyond the tariff windfall, Tesla's Q1 results were shaped by several genuine operational factors — some positive, some concerning.

Tailwinds: Services and Other gross profit grew, vehicle average selling prices rose (excluding FX impact), and per-vehicle costs fell on the back of lower material costs. Energy generation and storage also contributed meaningfully.

Headwinds: Vehicle deliveries of 358,023 units came in below the 365,000 analyst consensus and were approximately 7% lower than Q1 2025's 386,810 deliveries. Operating expenses also rose due to increased AI and R&D spending, CEO stock-based compensation from the 2025 award, and higher SG&A costs.

The delivery miss is particularly notable. Tesla produced 408,386 vehicles in the quarter — meaning inventory is building, not shrinking. That gap between production and deliveries is something to watch heading into Q2.

🔭 The BASENOR Take

Timeline: Q1 2026 results released April 22, 2026 | IEEPA refund portal opened April 20, 2026

Impact Level: High — affects how investors and analysts interpret Tesla's financial trajectory

Confidence: High on the numbers; Medium on the precise tariff refund amount (Tesla has not disclosed it)

Fred Lambert's question cuts to the heart of what matters for Tesla's long-term story. A 136% jump in operating income sounds transformational — and it would be, if it were driven by operational efficiency, volume growth, or margin expansion. But when the company's own earnings materials point to one-time items as the primary cause, investors and owners should recalibrate their expectations for Q2 and beyond.

The tariff refund story is also not uniquely Tesla's. Any U.S. company that paid IEEPA tariffs on imported components could be booking similar one-time benefits following the Supreme Court ruling. What makes Tesla's case notable is the scale — and the fact that the company chose not to quantify it separately, making it harder for analysts to model the underlying business.

The more structurally important question for Tesla owners and long-term watchers: can Tesla grow deliveries in Q2? The Model Y refresh, ongoing price positioning, and the ramp of new products will matter far more to the company's sustainable profitability than a one-time tariff windfall. With inventory building and delivery volumes still below year-ago levels, the operational pressure is real — regardless of what the headline earnings numbers suggest.

David covers the EV industry, regulatory developments, and accessory ecosystem. 15+ years writing about consumer tech. Based in London.

Sources verified at publish time. Spotted an inaccuracy? Email editorial@basenor.com.