The News: Tesla reported a Q1 2026 earnings beat of $0.41 per share, but the headline number obscures a more complicated picture — one-time warranty and tariff benefits were the top driver of profitability, and the CFO confirmed negative free cash flow is expected going forward.

Why It Matters: For Tesla owners and investors alike, understanding what's actually driving the numbers — and what isn't sustainable — matters far more than the surface-level beat.

Sources: @FredLambert · @wholemars on X, April 22, 2026

Tesla Q1 2026 Earnings: The Numbers Wall Street Missed

Tesla's Q1 2026 earnings report landed on April 22, and the headline reaction was predictably bullish — a $0.41 earnings-per-share beat tends to do that. But dig even slightly beneath the surface and a more complicated story emerges: one built on one-time benefits, undisclosed accounting items, and a CFO who openly confirmed that negative free cash flow is on the horizon.

📊 Key Figures

| Metric | Value | Context |

|---|---|---|

| EPS Beat | $0.41 | Above consensus estimates |

| #1 Profitability Driver | One-time warranty & tariff benefits | Dollar amount not disclosed |

| FSD Subscription Growth (YoY) | +51% | Year-over-year, Q1 2026 |

| Free Cash Flow Outlook | Negative (confirmed) | CFO statement, Q1 earnings call |

The Earnings Beat That Needs an Asterisk

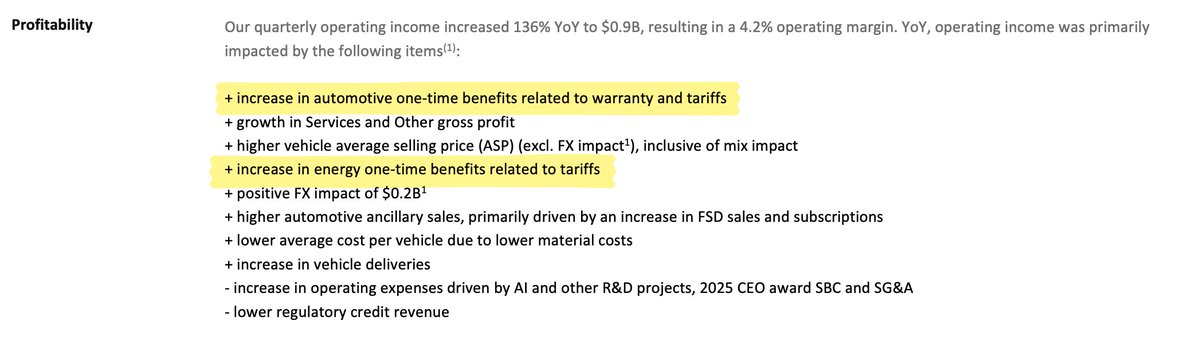

Tesla listed "one-time warranty and tariff benefits" as the single biggest driver of Q1 profitability — and then declined to disclose how large those benefits actually were. That's a significant red flag for anyone trying to model Tesla's underlying earnings power. A one-time benefit, by definition, doesn't repeat. If it's the top line item driving a beat, the beat itself becomes structurally hollow.

The tariff angle is particularly notable. Tesla appears to have booked benefits related to IEEPA tariff treatment — the specifics of which were not elaborated on during the call. Without knowing the dollar magnitude, analysts and investors are essentially being asked to trust a number they can't verify or strip out.

The One Genuinely Bright Spot: FSD Subscriptions

Amid the earnings quality concerns, there's one data point that stands on its own without caveats: self-driving subscription growth hit 51% year-over-year. That's a real, recurring revenue signal — and it matters.

FSD subscriptions represent the kind of high-margin, software-driven revenue that Tesla's long-term bull case depends on. A 51% YoY growth rate suggests meaningful adoption acceleration — whether driven by improved capability, more aggressive pricing, or simply a larger installed base becoming subscription-eligible. For our FSD coverage, this is one of the most important metrics to watch quarter over quarter.

CFO Confirms: Negative Free Cash Flow Is Coming

Perhaps the most significant disclosure of the evening came not from the earnings release itself, but from the CFO's commentary: Tesla is expecting negative free cash flow going forward. This is a direct statement from management — not a bear-case analyst projection.

Negative FCF isn't automatically catastrophic — companies burning cash to fund growth can still be sound investments. But it does mean Tesla will be consuming rather than generating cash in coming quarters, which raises questions about capital allocation priorities: Gigafactory expansions, Robotaxi infrastructure, Optimus production scale-up, and more. All of these carry significant capex requirements.

🔭 The BASENOR Take

Timeline: Q1 2026 earnings reported April 22, 2026

Impact Level: 🟠 Medium-High — Affects investor sentiment and Tesla's near-term capital strategy

Confidence: High — CFO statements and official earnings disclosures are primary sources

Analysis: The market's initial positive reaction to the EPS beat likely reflects headline-reading algorithms and momentum traders rather than fundamental analysis. The combination of undisclosed one-time benefits as the primary profit driver, plus a management team openly guiding to negative free cash flow, paints a picture of a company in a heavy investment cycle — not a profitability inflection. The 51% FSD subscription growth is the one number that genuinely supports the long-term software revenue thesis, but it's not yet large enough to offset the near-term cash burn story.

📰 Deep Dive

The core tension in Tesla's Q1 2026 report is between what the market sees and what the numbers actually say. A $0.41 EPS beat is a clean, simple number that triggers algorithmic buying. What doesn't trigger that same response is the disclosure — buried in the earnings materials — that the top driver of that beat was a category of benefits Tesla chose not to quantify. That asymmetry of information is a problem for anyone trying to assess whether Tesla's underlying automotive margin is recovering, stable, or continuing to compress.

The tariff benefit angle deserves particular scrutiny as trade policy continues to evolve. If Tesla booked IEEPA-related tariff relief as a one-time gain, that benefit is inherently tied to a specific policy environment. Any change in tariff structure — in either direction — could reverse or eliminate it. Booking it without disclosure of the magnitude makes it impossible for outside observers to stress-test the earnings against different policy scenarios.

On the FSD side, 51% year-over-year subscription growth is the kind of metric that, if it compounds, eventually becomes transformative for Tesla's financial profile. High-margin recurring software revenue is the business model Tesla has been promising for years. The question is whether the growth rate holds as the subscriber base grows larger and the easy early-adopter gains are exhausted — and whether the underlying FSD capability improvements continue to justify the subscription price for mainstream owners.

The negative free cash flow guidance is the headline that will matter most in coming quarters. Tesla is clearly in an investment phase, and management is being transparent about it. But transparency about cash burn doesn't make the burn less real. Owners and investors should watch Q2 capex figures closely — the gap between Tesla's ambitions across vehicles, energy, autonomy, and robotics is wide, and bridging it while FCF is negative requires either debt, equity, or a faster-than-expected revenue ramp from new products.

Marcus covers Tesla's software releases, FSD rollouts, and OTA changes. Background in automotive engineering. Based in Austin.

Sources verified at publish time. Spotted an inaccuracy? Email editorial@basenor.com.